The Halo Effect of Food Halls:

Understanding The True Value for Developers

A busy food Hall drives incremental value for developers.

When developers underwrite a food hall, most of them model one revenue stream — the food hall's own P&L. That standalone analysis is fair, and the math holds up. A healthy food hall delivers 8 to 12 percent EBITDA on gross revenue, which justifies the food hall as a real estate investment on its own merit. We walked through that math in our recent piece on food hall economics.

But the standalone P&L is one layer of the value a food hall creates. There is a second layer — and for most developers, it is the layer that matters more.

The second layer is the halo effect on the surrounding real estate. A well-designed, well-operated food hall lifts the value of every other revenue line in a development: residential rents in adjacent buildings, ground-floor retail rents, office leasing pace, hotel ADR and occupancy, asset cap rate at refinance or sale. The published research from major commercial real estate bodies — ICSC, JLL, CBRE, Cushman & Wakefield, NAIOP — is consistent and directionally unambiguous. Food halls function as halo-effect amenities. The magnitude varies by market and asset class, but the direction is documented.

This piece is for developers, REITs, mall owners, hotel sponsors, and stadium operators who are evaluating whether to include a food hall in their next project. It walks through what the published research supports, how the math works across four common development contexts, and how to underwrite the halo effect honestly in your pro forma. The goal is to give you the permission and the framework to model both layers of value — not just the standalone food hall return.

If you are early on a project and want a clear-eyed read on whether a food hall fits, that is the conversation we are built to have.

The Two Layers of Value

Before we discuss the halo effect, it's worth being clear that food halls are real investments in their own right. A healthy mid-sized urban food hall typically delivers 8 to 12 percent EBITDA on gross revenue, with operating expenses running 28 to 32 percent inclusive of labor. Strong urban flagships run at the upper end of that range; neighborhood halls in softer markets run below it. These returns are defensible without the halo effect, and they justify the food hall as a real estate investment on its own merits.

But the standalone P&L is only one layer of what a food hall delivers. There are actually two distinct layers of value that these assets create:

Layer One — the standalone Food Hall P&L. Revenue from vendor commissions, the beverage program, events and group dining, programming, delivery, sponsorship, and ancillary lines. Operating expenses, including labor. The net result is the rent and EBITDA the food hall produces as a standalone business.

Layer Two — the halo effect on surrounding real estate. The lift the food hall generates on every other revenue line in the development. Residential rent premiums in adjacent buildings. Ground-floor retail rent lift. Office leasing velocity. Hotel ADR and occupancy. Asset-level cap rate compression at refinance or sale.

Most pro formas only model Layer One. All of the benefits of Layer Two — the lift on residential rents, retail rents, hotel ADR — get assumed away, remain untracked, or get quietly omitted.

The point of this article is to give developers and retailers an honest framework for modeling Layer Two, so the food hall's full value to your project shows up in your pro forma.

How the Math Works Across Different Classes

The halo effect plays out differently in different assets. The underwriting logic is the same in each case — you count the food hall's standalone EBITDA plus the lift it generates on the surrounding real estate — but the specific channels of lift vary.

Here are four different asset types where the food hall has the most obvious lift:

1. Malls and Shopping Centers

This is where the food hall format is most precisely calibrated to its setting. The reason is dwell time — not just that food halls increase it, but that they increase it to the right amount. A well-run food hall delivers a typical guest dwell time of 26 to 32 minutes. That number matters in two specific ways for retail centers:

For office workers and downtown lunch traffic, 26 to 32 minutes fits inside a standard lunch break. The guest can get in, eat well, and get back to work without burning a full hour. That makes a food hall an everyday option for the working population around the center.

For shoppers, that duration is calibrated to refresh without ending the trip. A 75-minute sit-down a la carte lunch transitions a shopper from active shopping mode into "I'm tired, let's go home" mode — killing the second-half retail spend. A food hall refreshes the guest while keeping them in shopping flow. That is exactly the behavior shopping center owners are trying to engineer.

This dwell-time calibration is why the ICSC/JLL global F&B study found that the presence of well-positioned F&B clusters drives both foot traffic and overall scheme sales — and why the share of mall space allocated to F&B has grown from 5 percent a decade ago to 10-15 percent today in the UK, with new destination schemes allocating up to 25 percent. Mall owners aren't just replacing dying department store anchors with food halls because they need the space filled. They are doing it because the data supports the format as a stronger traffic generator and a better, more targeted dwell-time amenity than the anchors it replaces. Getting the design right is what makes the difference between a food hall that captures the halo effect and a food court that undermines it — we walk through the specific design principles that separate the two in our food hall design essentials post.

CBRE's published view is consistent — they describe food halls as a "high-impact amenity for improving a property's dwell time, leasing velocity, and NOI." Cushman & Wakefield's research reaches the same conclusion. The directional research is unambiguous; food halls work as halo-effect amenities for retail centers, and the dwell-time profile is the specific reason why.

2. Stadiums, Arenas, and Entertainment Venues

Food halls work at sports and entertainment venues — but only in specific contexts. The format is built for everyday traffic, not exclusively for event-day traffic.

A food hall at an arena in a dense urban core works because the surrounding downtown supports it 365 days a year. The model works at venues like Capital One Arena in Washington DC, Madison Square Garden in New York, Climate Pledge Arena in Seattle, and T-Mobile Center in Kansas City — places where the surrounding office, residential, and tourist density generates enough everyday demand to carry the food hall through non-event days.

The model does not work at suburban stadium districts that only activate on event days. A food hall needs everyday traffic — the office workers, the residents, the tourists, the lunch crowd — to sustain vendor revenue, justify staffing, and maintain the bench of vendors that keeps the curation fresh. Event-only traffic isn't enough to support the operating cadence the format requires.

The asset class that works isn't "stadiums" broadly — it's "urban-core venues with surrounding 365-day demand." For those venues, the halo effect compounds because the food hall extends visit duration before and after events (capturing more guest spend per visit) AND drives off-season visitation that pure-event venues can't sustain. Both layers of value show up.

3. As a Complement to Hotels (especially select-service hotels)

A Merchandised Food Hall Stall

This is the asset class where the underwriting math is sharpest, because select-service and limited-service hotels are operationally designed to minimize their F&B program. According to published hospitality industry research, F&B contributes only about 7.4 percent of total revenue at select-service hotels, compared to roughly 28.8 percent at full-service hotels.

That low F&B share isn't an accident. It's a deliberate choice. Select-service hotel operators stay out of meaningful F&B because the operating burden, staffing complexity, and capital expense of running restaurants don't fit their service model. The result: a select-service hotel guest gets a great room at a price meaningfully below a full-service hotel, but with an unmet F&B need.

An adjacent food hall fills that unmet need without requiring the hotel to build or operate restaurants. The guest experience moves toward what full-service hotels deliver — without the hotel taking on the operating risk of F&B. The halo effect shows up in two specific ways:

ADR lift. The hotel can credibly move its daily rates closer to its full-service comparables because the guest experience now includes meaningful walkable F&B. Peer-reviewed research on the importance of F&B in U.S. hotel operations documents that F&B investment positively affects ADR, RevPAR, and GOPPAR.

Occupancy lift. Adjacent amenity quality drives guest satisfaction, online reviews, and repeat booking rates. Even small lifts in occupancy compound meaningfully against the room revenue base.

For a developer with two select-service hotels in a mixed-use project — say, 240 total rooms at $150 ADR and 70 percent occupancy — even a conservative 5 percent ADR lift combined with a 3 percent occupancy lift can generate hundreds of thousands of dollars of annual revenue on the hotels alone. Layer that on top of the food hall's standalone EBITDA, the residential rent premium on the project's apartments, and the retail lift on the project's ground-floor space, and the food hall starts to pay for its buildout before the food hall's own P&L generates a meaningful dollar.

4. Mixed-Use Developments

Mixed-use is where the halo effect compounds across the most revenue lines simultaneously. A well-positioned food hall in a mixed-use project can lift:

Residential rents in adjacent buildings. The best-documented analog is the Zillow Research study on Whole Foods and Trader Joe's, which analyzed 17 years of data across nearly 3 million homes around 451 Trader Joe's and 375 Whole Foods locations. Homes within a mile of these anchor amenities had higher median values than comparable homes citywide — and critically, homes appreciated faster after the store opened, suggesting the amenity itself drives the premium rather than the store choosing already-expensive areas. RCLCO Real Estate Advisors documented a 5.8 percent rent premium for properties with ground-floor Whole Foods or Trader Joe's anchors. The functional logic of a food hall is identical to a grocery anchor: a daily-traffic-generating amenity that makes the surrounding properties more walkable and more desirable.

Ground-floor retail rents on adjacent space. The ICSC/JLL global F&B study, commissioned by the trade body for shopping center real estate, found that well-curated F&B clusters drive foot traffic growth, dwell time, and overall scheme sales. Adjacent retail tenants benefit directly from that lift.

Office leasing pace. Modern Class A office tenants — particularly those in talent-driven industries — underwrite walkable amenity access into their site selection. A food hall as an integrated amenity for the surrounding office buildings can meaningfully accelerate leasing velocity and improve tenant retention. NAIOP's coverage of experiential retail describes this dynamic in the broader context of experience-driven anchor strategies.

The compound effect across residential, retail, and office in a single mixed-use project is the reason food halls are increasingly being underwritten as integrated amenities rather than standalone investments in this asset class.

This is the math that gets a food hall approved in a development committee. It is also the math that most pro formas omit.

The Underwriting Framework

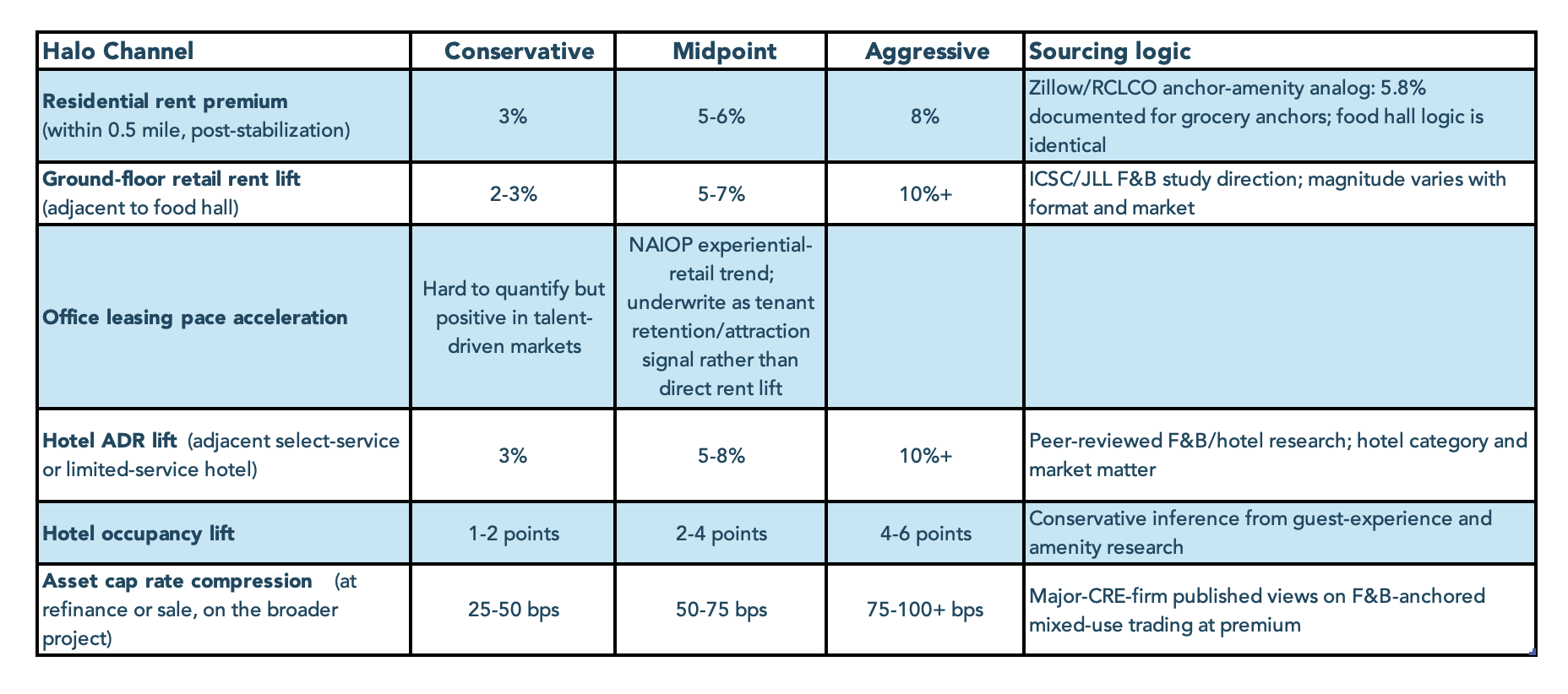

The published research is directionally unambiguous about the food hall halo effect. The magnitude is harder to pin down with a single number, because it varies by market, by asset class, by the quality of the food hall design and operation, and by the strength of the surrounding submarket.

Rather than quote single numbers that don't survive scrutiny, we offer a model with sensitivity bands — conservative, midpoint, and aggressive scenarios for each halo channel — allowing you to run your project underwriting against all three.

Here is a working framework based on the published research and our operating experience:

Food Hall Underwriting Framework Grid

A few principles for using this framework:

Run all three scenarios. A pro forma that only models the aggressive case is fragile. A pro forma that only models the conservative case may not justify the project. The decision usually lives in whether the midpoint pencils.

Conservative is more credible than aggressive. When the conservative case still produces a meaningful project-level return, the project is robust. When the project only pencils on the aggressive case, the project is fragile.

Underwrite the halo on a long-dated basis. The halo doesn't fully arrive in year one. Residential rent premiums show up at lease renewal. Retail rent lift shows up at lease rollover. Hotel ADR lift develops over the first 18-36 months of the food hall's operation. Underwrite the lift across a 3-5 year horizon, not at stabilization-day-one.

Treat the food hall's standalone EBITDA as the floor, not the ceiling. The food hall's own returns should justify the project on a worst-case basis. The halo effect is the upside that makes the project compelling.

That framework gives you a defensible way to underwrite both layers of value in your pro forma. It's how to model the halo effect honestly — without overclaiming, and without omitting it. This is also the foundation for Onset’s Food Hall Consulting Services.

The Halo Effect Doesn't Happen Automatically

This is the part of the analysis that gets understated in most published coverage of food halls. The halo effect on surrounding real estate isn't automatic. It is a function of how the food hall is designed, programmed, and operated.

A poorly designed or poorly run food hall doesn't deliver the halo. In some cases, it actually erodes the value of the surrounding real estate — a half-empty food hall sends the opposite signal of a well-curated one, and the surrounding properties absorb that negative signal in their leasing conversations.

The factors that determine whether a food hall actually delivers the halo:

Couple carrying a tray of food

Vendor curation that serves the surrounding submarket. A food hall built for a downtown office crowd looks different than one built for a residential neighborhood, which looks different than one built for a tourist destination. The wrong curation can kill the halo before it starts.

A real beverage program. The bar isn't just a food hall revenue line — it's the social anchor that drives dwell time, repeat visits, and the destination value the surrounding real estate benefits from. An underbuilt bar shortens dwell time and weakens the halo.

Programming and activation as a continuous operating function. A food hall that's quiet on Tuesday and Wednesday nights doesn't drive the everyday traffic the halo requires. Programming has to be calendared, budgeted, and owned — not improvised.

Marketing as an ongoing channel, not a launch tactic. The food hall's brand recognition is what the surrounding real estate is leasing into. A food hall that goes silent after opening softens its own marketing power and the halo it generates.

Vendor turnover discipline. Dark stalls signal a struggling hall. A struggling hall doesn't lift the surrounding real estate; it pulls it down. Operators who run a continuous vendor recruiting pipeline don't have dark stalls. Operators who don't, do.

We covered these operating disciplines in detail in our piece on food hall economics and in our guide on how to choose a food hall operator. The reason they matter for the halo conversation is simple: the halo effect is the operator's deliverable, not the developer's. The developer builds the hall; the operator delivers the halo through how the hall is run.

If you are underwriting the halo effect in your pro forma, you are implicitly underwriting the operator who will run the hall. The operator you hire determines whether you capture the halo or leave it on the table.

Developer takeaways

If you are evaluating a food hall in a mixed-use development, a mall, an urban-core sports or entertainment venue, or as a complement to a select-service or limited-service hotel, the halo effect is a real line of value worth modeling. Most developers underwrite only the food hall's standalone P&L. Doing both layers — the standalone return AND the halo on the surrounding real estate — gives you a meaningfully more complete picture of what the food hall actually contributes to your project's total ROI.

If you are early on a project and want a clear-eyed read on whether a food hall fits — and how the halo effect would model in your specific context — that is the conversation we are built for. We can walk you through the underwriting framework against your actual project, your actual asset class, and your actual market.

FAQ

-

The halo effect of a food hall is the lift it generates on the value of surrounding real estate — residential rents in adjacent buildings, ground-floor retail rents, office leasing velocity, hotel ADR and occupancy, and asset-level cap rate at refinance or sale. The published research from major commercial real estate bodies including ICSC, JLL, CBRE, and Cushman & Wakefield confirms that well-positioned food halls function as halo-effect amenities. The magnitude varies by market and asset class, but the direction is documented.

-

The best-documented analog comes from research on Whole Foods and Trader Joe's anchor amenities. Zillow's 17-year analysis of nearly 3 million homes found that properties within a mile of these anchors appreciated faster after the store opened than comparable homes citywide. RCLCO Real Estate Advisors documented a 5.8 percent rent premium for properties with these ground-floor anchors. Food halls function as the same kind of daily-traffic-generating amenity; the underwriting analog is credible even though food-hall-specific studies are still emerging.

-

Yes — and the dwell-time calibration is the specific reason why. A food hall delivers a typical guest dwell time of 26 to 32 minutes, which fits a standard lunch break for office workers and is calibrated to refresh shoppers without ending their shopping trip. A 75-minute restaurant meal transitions a shopper into "let's go home" mode and kills second-half retail spend. A food hall refreshes the guest while keeping them in shopping flow. The ICSC/JLL global F&B study found that well-positioned F&B clusters drive both foot traffic and overall scheme sales.

-

Food halls work at arenas and entertainment venues located in dense urban cores — places like Capital One Arena in Washington, DC, Madison Square Garden in New York, Climate Pledge Arena in Seattle, and T-Mobile Center in Kansas City — where the surrounding downtown generates 365-day demand. The format does not work at suburban stadium districts that only activate on event days. The food hall needs everyday traffic from the surrounding office, residential, and tourist density to sustain vendor revenue between events.

-

Select-service and limited-service hotels are operationally designed to minimize their F&B programs — they generate only about 7 percent of revenue from food and beverage compared to roughly 29 percent at full-service hotels. That low F&B share is a deliberate choice that leaves a meaningful guest need unmet. An adjacent food hall fills that need without requiring the hotel to build or operate restaurants, which allows the hotel to credibly price closer to its full-service comparables and to drive higher guest satisfaction, online reviews, and repeat booking rates. Peer-reviewed research on U.S. hotel operations confirms that F&B investment positively affects ADR, RevPAR, and GOPPAR.

-

Use sensitivity bands rather than single numbers. Run conservative, midpoint, and aggressive scenarios for each lift channel — residential rent premium, retail rent lift, hotel ADR lift, occupancy lift, and cap rate compression. Treat the food hall's standalone EBITDA as the floor of the project model and the halo effect as the upside. Underwrite the lift across a 3-5 year horizon rather than at stabilization day one, because residential premiums show up at lease renewal, retail lift shows up at rollover, and hotel ADR lift develops over the first 18-36 months. A conservative-case project that still pencils is robust; a project that only pencils on the aggressive case is fragile.